Some thoughts on KRW underperformance since early May

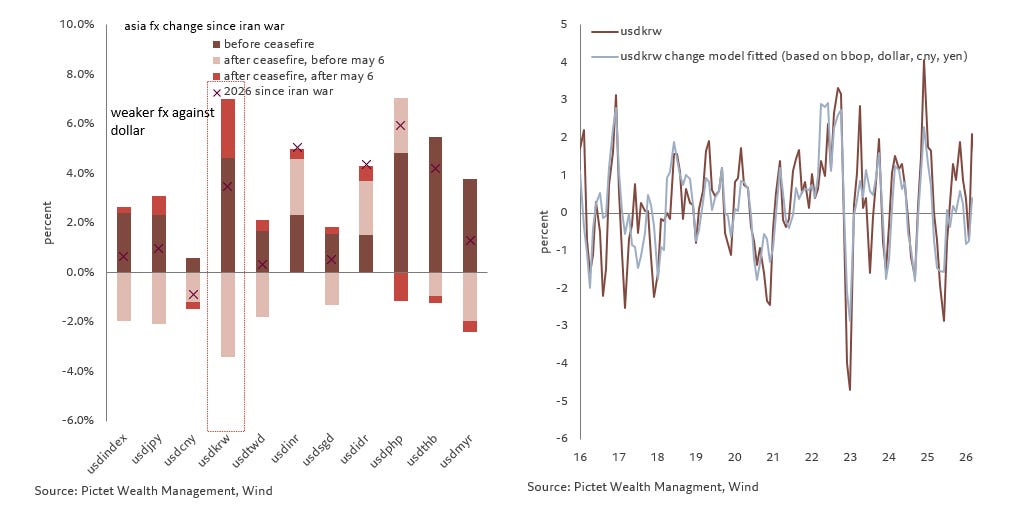

KRW was one of worst performing Asia currencies in March after Iran war, but followed by strongest rebound after the ceasefire in early April. However, it has again underperformed since early May, down by around 2% against dollar.

Key question is, would KRW underperformance continue in coming months?

Short answer is no, as I think factors driving recent underperformance would not sustain and positive factors could outweigh to support KRW in coming months.

As I shared previously, I organize my thoughts on KRW with a simple model of USDKRW on basic balance of payment (BBOP) and three major anchoring currencies-- dollar, USDCNY, USDJPY, and this model has explained KRW moves pretty well historically. When residuals are relatively large, it could suggest significant deviation of KRW from fundamentals with more speculation (like last year since August), and authorities could voice concerns and more likely take stabilization measures.

With this simple framework, since early May, significant foreign equity outflow has been the most important driver of KRW underperformance.

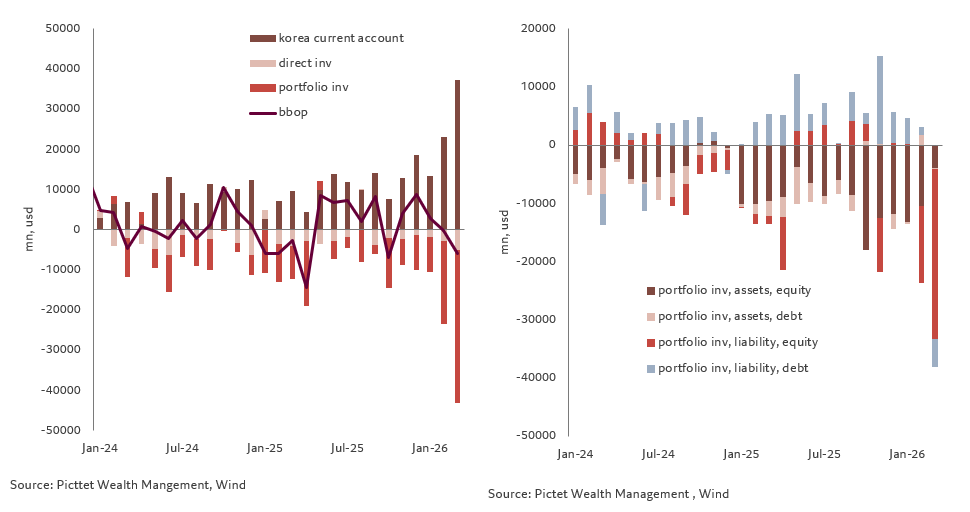

Since late last year, equity flow has been one of most important drivers of USDKRW. In H2 last year, it was significant retail equity outflow that weighed on KRW, along with high beta to yen (amid weaker yen), and also dollar hoarding with procyclical expectation, even with strong current account surplus.

Since March, retail equity outflow has reduced sharply, and current account surplus has been even stronger, but it was significant foreign equity outflow in March, along with high beta to dollar (and yen), and high imports of oil to GDP (large impact from term of trade shock), that pushed KRW to weaken the most in March (speculation probably also contributed).

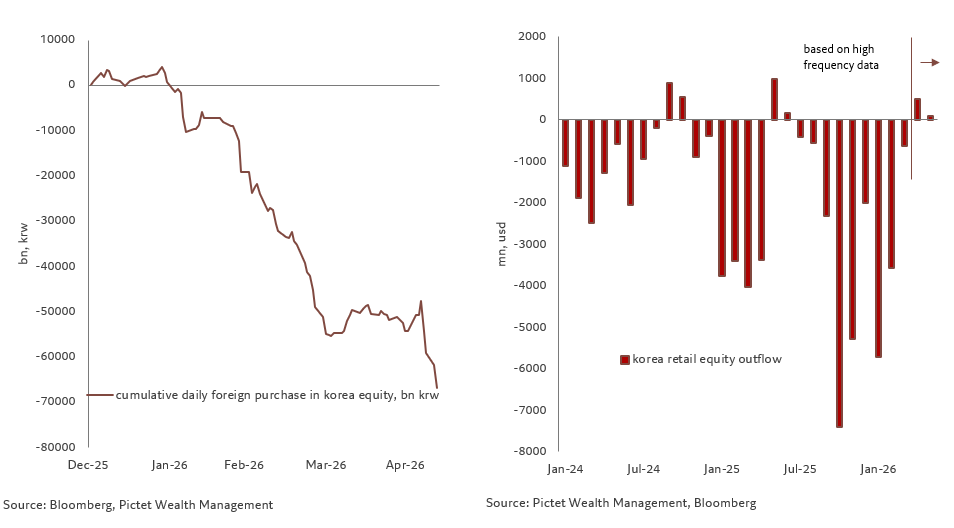

Since early May, foreign equity outflow has picked up significantly again (probably some profit taking, but retail investors flow actually more than offset that, supporting Korea equity ) after stabilization in April, with retail equity outflow likely still mild based on high frequency data and trade surplus likely still decent.

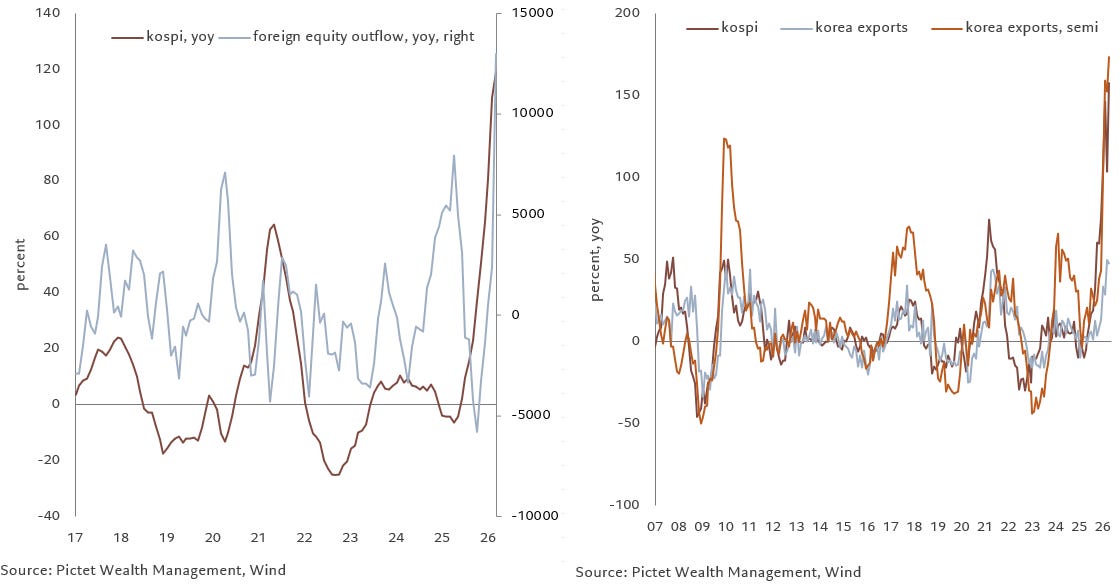

One key question is, would such significant foreign equity outflow sustain, with continued upside in Korea equity (which I shared previously given high correlation between Korea equity and tech exports which could be still decent in coming months supported by further chip price gains)?

I think likelihood is not high. One simple exercise is to look at correlation between Korea equity and foreign equity outflow. And while correlation is not strong, it suggests the higher Korea equity, the less foreign outflow, or at least it does not suggest the higher Korea equity, the more foreign outflow.

Another key question is, could strong current account surplus continue in coming months?

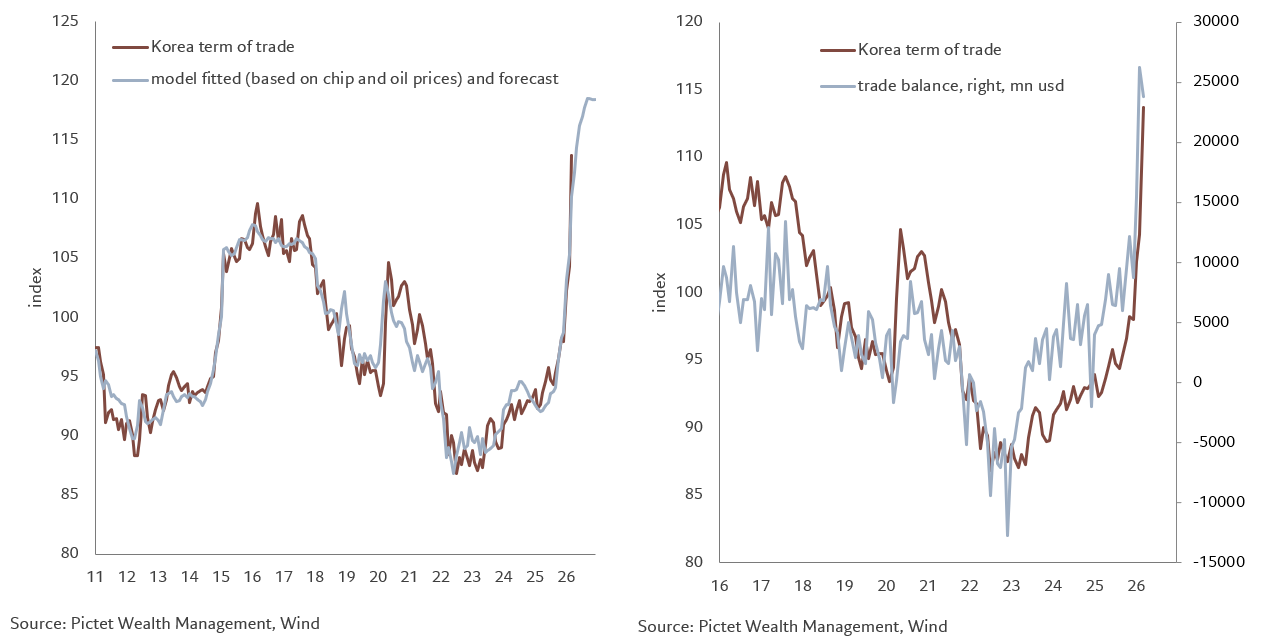

Yes, with further improvement in term of trade. Korea’s term of trade has improved significantly since late last year with surge in chip prices. For March, even with sharp increase in oil prices, term of trade improved further, suggesting gains in chip prices outweighed negative impacts from oil prices (and beta of term of trade to chip prices up in recent years).

And based on my model of term of trade on chip prices and oil prices, and my assumption for future path (chip prices could go up further, though at slower pace, and oil prices could gradually moderate in H2), term of trade could improve further, supporting robust current account surplus.

And in term of direction of anchoring currencies, as I shared, I expect RMB to appreciate mildly against dollar. And I am cautious on Yen, but with intervention risk lingering, downside could be capped to some extent.

In addition, authorities may take additional stabilization measures like they did in recent months if they perceive KRW significantly deviating from fundamentals. For instance, Korea’s Finance Ministry today said volatility in the FX market is increasing excessively compared to the economic fundamentals with a rise in overseas speculative trading.

Overall, I am still positive on KRW, though there remains risk from equity flow.