May RBA recap: hawkish reaction function reaffirmed, more hike likely (and needed)

RBA raised cash rate to 4.35% as widely expected, the third consecutive hike since February, as “inflation is likely to remain above target for some time and that the risks remain tilted to the upside, including to inflation expectations”.

RBA was the first DM central bank (except BOJ) to start hiking even before Iran war and also the first to hike in response to oil shock. Behind its hawkishness, it is unfavorable inflation profile that had already been too high and unacceptable before the war with excess demand, and oil shock has added fuels to fire.

I think there are three key messages from the meeting regarding future policy path:

Hawkish reaction function towards inflation reaffirmed

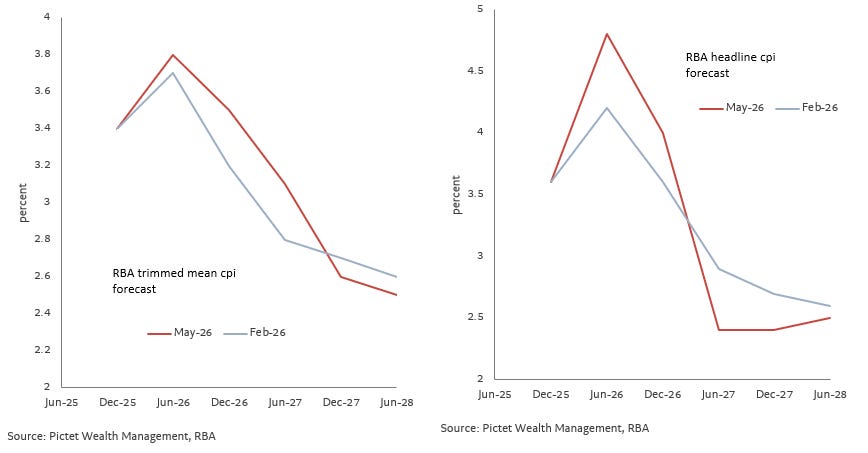

1) Even after significant upward revision in inflation, RBA remains concerned with upside risk, including inflation expectation. RBA not only revised inflation upwards, but also delayed timing of trimmed mean inflation back to target range a bit further (from H1 27 to H2 27). If February forecasts were already unacceptable, basically there would be no room to tolerate for any upside. And RBA flagged indications of second order effects on inflation and mentioned passthrough from oil shocks could be faster. Meanwhile short-term inflation expectation has increased further, and RBA assumed long term inflation expectation to remain anchored around inflation target over the medium run, which is more likely to subject to upside risk than downside.

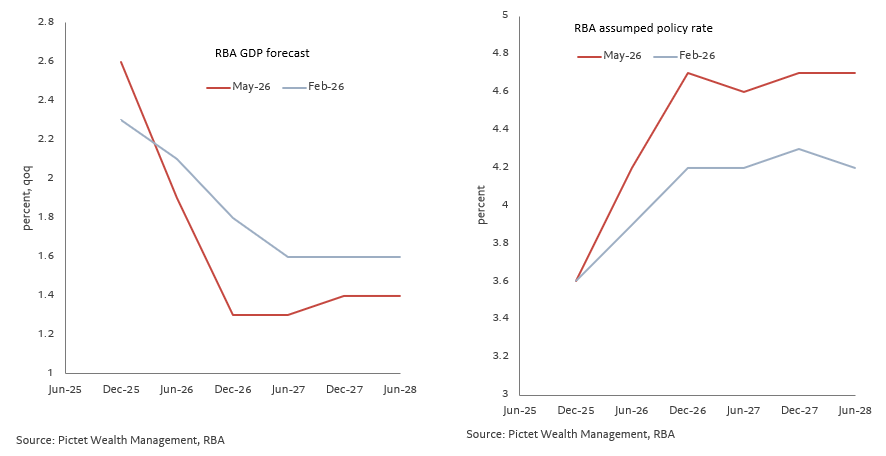

2) RBA viewed negative impact from the war on growth relatively limited in baseline. RBA listed several reasons and mentioned impacts from oil shock could be even neutral or positive for Australia (net energy exporter). And while RBA revised GDP growth downward, it to a large extends was due to higher assumed policy rate and reassessment of consumption momentum before the war. And while oil shock has put many central banks in a difficult position to balance between inflation and growth, it seems to be less challenging to RBA.

3) Governor Bullock has made very clear in the presser that weight of inflation in reaction function is currently larger (than growth) given higher risk in inflation. And this should be not a surprise, especially with Bullock spending much time in the presser about costs of high inflation and its impacts on inflation expectation, and importance of bringing inflation back to target.

More hike likely and needed to get inflation back to target as currently forecast

1) With additional pressure from oil shocks, additional 50bps hikes before end 2026 compared to February forecasts were assumed and needed (cash rate 4.2% vs 4.7%) to make sure inflation back to target as they are forecasting. And unless inflation surprises to downside significantly in coming months (which seems to be hard), or growth deteriorates more than expected, with little upside to tolerate, at least another hike is needed.

2) With higher neutral rate, confidence in monetary policy being sufficiently restrictive to take inflation back is still not strong enough. RBA has revised their estimates of neutral rate higher, and in May viewed policy rate at 4.1% sits within and near top of range, and 4.7% is slightly above the range. Bullock in the presser also mentioned 4.35% may not be as restrictive as it was two to three years ago when cash rate was at same level . And also RBA mentioned, these estimates are made by adding long term inflation expectation which has been relatively stable. And if putting more weight on short term inflation expectation, which is higher and has been rising, neutral rate could be even higher and cash rate could be less restrictive. And beyond policy rate, RBA mentioned extent to which financial conditions are restrictive remains uncertain (e.g. funding and credit growth).

A near-term pause followed by further cut, but risk for fourth consecutive hike

There are some signs, especially from press conference, that RBA may want to pause after three consecutive hikes before hiking again.

When asked if RBA is on a wait and watch mode from here, governor said, “wait and watch is probably a wrong term, but…we feel we are now in a position where we’ve got space to be alert to both sides of risks to inflation”.

And when asked to explain about 8:1 vote, governor said “… those who voted for hike were also of the view that this puts us now in a good position to just observe now what is going to happen with wars, prices and employment.”

In addition, in the forward guidance part of the statement. “having raised the cash rate three times…” was also added.

Overall, I think RBA may want to pause for a while to observe more data, but given what I discussed above, they will hike, at least one more. At this point, I expect August, and risk for earlier and fourth consecutive hike in June is higher than being delayed to September.